1Q22 in Startupland: Is the Seed Stage Valuation Slowdown Happening?

1Q22 in Startupland: Is the Seed Stage Valuation Slowdown Happening?

Everybody “knows” that the global conjuncture and public market performance are determining a slowdown in the US startup market. But, is it true? A closer look at the Seed Stage.

The first quarter of 2022 is behind us, and everybody knows that lot of changed since Q4 2021. Since January, valuations and VC investments slowdown have been all over the news on Twitter. The public market is going down while the Russia-Ukraine war threatens to escalate to a global conflict.

As many of you know, we invest in Pre-Seed and Seed stage companies in the USA, with a clear preference for Silicon Valley—where we placed our HQ. We have no stats or sophisticated reports to show, but we observe what’s happening on the field, and I must say that not that much has changed since 2021. In Q1, six companies joined our portfolio, with valuations consistent with the previous year's trend:

Rare Pre-Seed—good—opportunities

Seed rounds at $20M post and above

Seed extensions between $50M and $90M.

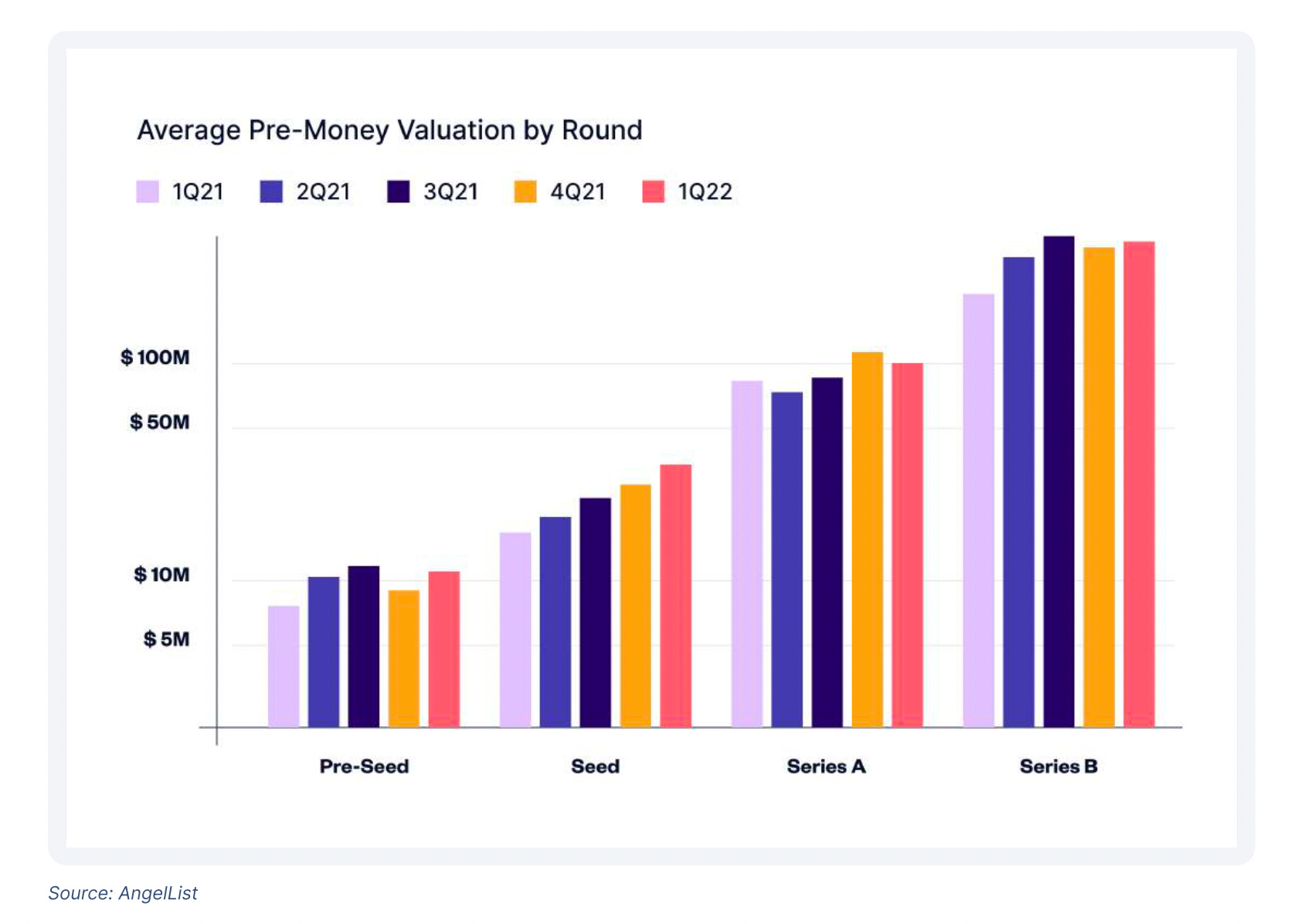

That doesn’t look like a slowdown at all, and if we analyze the AngelList Q122 report, we see it clearly:

Following the AngeliList Report data, Series A fell off by 5.5% in a pre-money valuation, and Series B increased 1.8%. Meanwhile, at the Seed stage, Pre-Seed valuations jumped 21% to $10.8M, and Seed rounds saw an even bigger increase of 25% to $34.3M.

That suggests two important things:

Public market trends have little or no influence on early-stage valuations

Global conjunctures are not considered a threat for now.

That means the US market underestimates what’s happening around us, or early-stage is considered so far from the liquidity event that valuations won’t be impacted in the near term.

AngelList Venture report states this fact based on its data with thousands of companies in the portfolio:

As we’ve written in the past, public and private market performance appear to be uncorrelated. This quarter’s performance is another piece of evidence to support that theory.

And that would explain what we observe as a direct experience in today’s market. We heard many operators talking about a slowdown in the later-stage investment—and I think it’s happening—but we can’t say the same for the Seed stage.

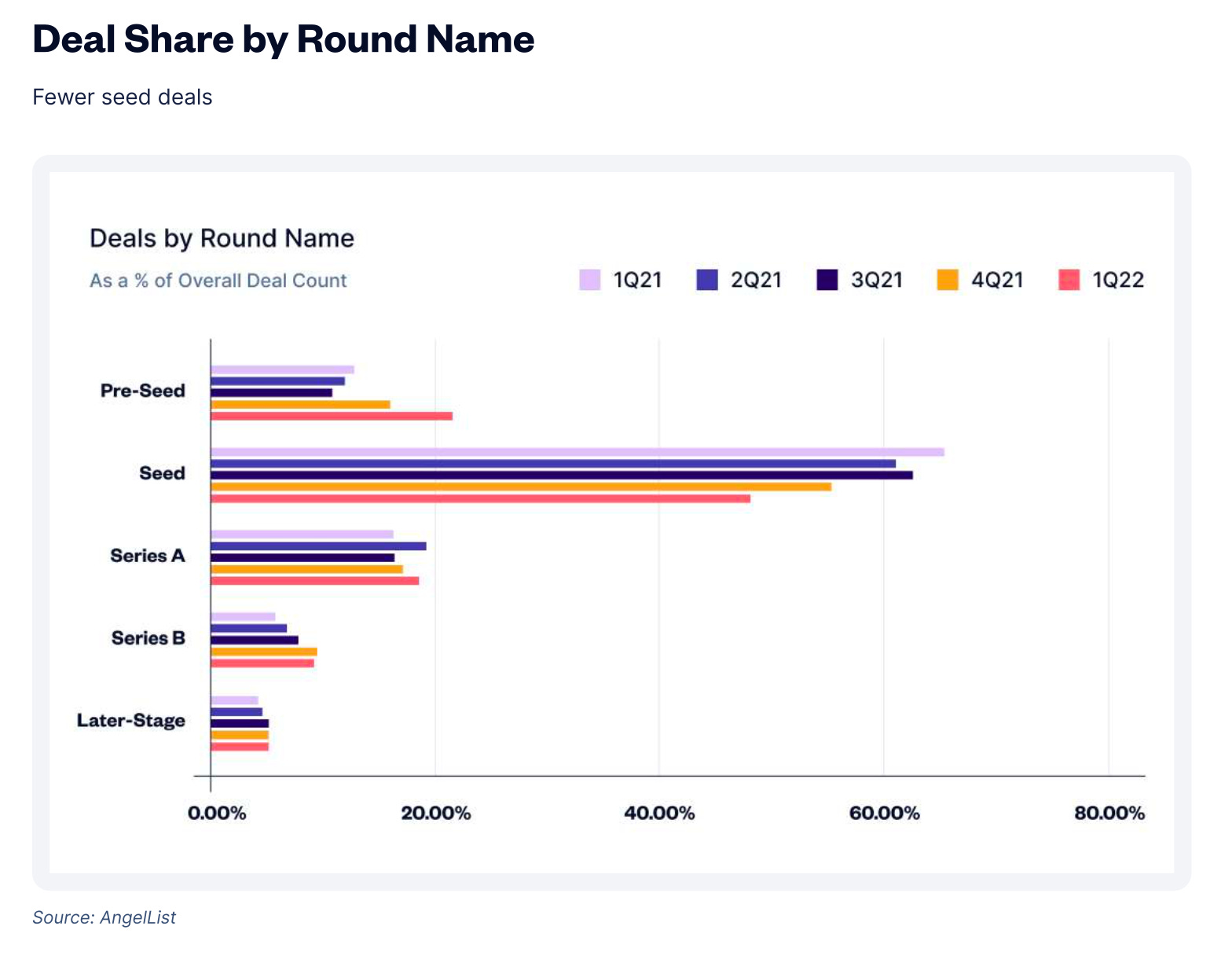

According to AngelList Venture, what changed compared to the previous year is the number of deals at the Seed stage:

1Q22 saw a precipitous decline in the number of seed-stage deals on the platform. Compared to 2021, when roughly 60% of deals occurred at the seed stage, only 48% of deals on AngelList occurred at the seed stage in 1Q22.

That means valuations keep growing, and investors write fewer and bigger checks to invest at the seed stage. They seem to like to deploy capital in even younger companies in the Pre-Seed stage.

Part of the uncontrolled increase in companies’ valuation—that it’s still a reality—directly results from moving online the fundraising process. More and more investors worldwide can now deploy capital, which created a background noise for professional investors moving the valuation cap upward.

We should consider a second factor affecting this uncontrolled valuations phenomenon. More and more big VCs are joining the Seed stage with dedicated funds. Hundreds of millions to be invested only in Seed companies might push companies’ valuation even higher in 2022.

Even if the increase in the company valuation—and the consequent less dilution when fundraising—might be perceived as an advantage for founders, we think it risks becoming a significant threat in the long run.

We are witnessing a dangerous phenomenon where the perception of value detaches from any sustainable reality based on provable results by too many multiples. The Late-stage investment has a reality check right now, and the Seed/Early stage will probably be the next.

Less than four years ago, you could invest $100K in a company and get almost 1% of its shares. Today that check is 3-4X for the same ownership. Companies that consistently grow around 20-25% MoM today want to raise Seed Extensions at almost $100M valuations. At the same time, we start to observe a slowdown in Series A/B rounds, and VCs that lead those rounds take more time to evaluate their investments.

The critical fact behind the phenomenon is that many 2021 investments in the early-stage market have been closed thanks to hedge funds that shifted their strategy aggressively into this space in the last three years. According to PitchBook, we are talking about 78% of venture dollars invested in 2021.

What will it happen if those non-traditional investors decide to pull the plug?

It will be interesting to observe the hedge fund strategy in Q2. Those investors might change their plan again—wait, it’s already happening—and companies’ valuation could be hopelessly compromised.

Tomasz Tunguz, Managing Director at Redpoint Ventures, wrote something interesting about this in a recent article:

The surge of hedge fund capital into Series C-E investing boosted median pre-money valuations by 150% in 2021.

And the first signal of the bad investment strategy in the later stage is here:

Tiger Global is having a year. According to a new report from Financial Times, the low-flying-yet-seemingly-ubiquitous 21-year-old outfit has seen losses of about $17 billion during this year’s tech stock sell-off. FT notes that’s one of the biggest dollar declines for a hedge fund in history.

According to the TechCrunch article mentioned above, Tiger Global invested a massive amount of capital also in the Q1 2022:

The 78 deals it led in the first quarter of this year [..] wound up in companies that collectively raised $7.6 billion, Crunchbase News reported last month.

So, plans are already changing:

Tiger Global apparently saw what was coming. Its team, which works as one unit to make both hedge fund and venture bets, had already all but abandoned late-stage venture deals by early February, as The Information reported that same month.

According to The Information, what will see is Tiger Global pulling back from pre-IPO companies and deploying more capital in the early stages—and they usually do that by writing considerable checks. That’s very dangerous because companies’ valuation might surge again when they should instantly decrease to absorb the market turmoil.

Softbank is another juggernaut found in many late-stage investment rounds in the last few years. They also reported a $26B loss in Q1 2022, and apparently, they decided to slow down their investment pace, according to PitchBook:

SoftBank is expected to cut its startup investment in this next fiscal year by more than half.

Something is happening, and founders must think twice before setting their valuation 🧢 too high, even if the abundance of capital and the scarcity of investment opportunities might keep valuations growing.

In the US, VC-backed companies pulled in more than $330 billion last year—nearly double the previous record of $167 billion set the year before. As the past three months have shown, this kind of performance is not indefinitely sustainable.

Multiples used to assign companies valuations will drop in the following months. It will probably take some time—six months, maybe—but the private market will likely follow the public market slowdown, as highlighted in this article by a16z:

However, the impact on venture markets will not be clear until data for the coming months and quarters filters in, and even then, many deals announced in Q2 were likely priced in Q1. In other words, it can take 6+ months before we see what impact the public market downturn has had on venture funding.

In conclusion

Investing in startups is a long-term game that can be easily compromised by either seeking or accepting a preposterous high valuation along the journey. Think about that risk starting from Pre-Seed, because, statistically speaking, in ten years, there’s a good chance that your company will go through at least one market slowdown—maybe two. Don’t be greedy and follow a sustainable valuation path, and you will always be correct.